Expected Value: Probability Math and Overlay Identification

Three years into my career I went through a brutal losing run — 47 bets, not a single winner. My staking was disciplined, my bankroll survived, but my confidence was destroyed. A more experienced analyst looked at my records and said something I have never forgotten: “Your strike rate does not matter. Your expected value does.” He was right. When I reviewed those 47 bets, the prices I had taken implied average probabilities well below my own assessments. I was backing value. The variance caught up eventually, and the next 100 bets produced a 14% ROI. The maths had been working the whole time.

Value betting is not about picking winners. It is about identifying situations where the odds offered by the bookmaker underestimate a horse’s true chance of winning. Total betting turnover on UK horse racing dropped 4.3% in 2025 and 10.7% versus 2023 — the shrinking market means bookmakers are competing harder for active customers, which occasionally creates pricing inefficiencies that a disciplined punter can exploit.

The Expected Value Formula Applied to a 10-Pound Racing Bet

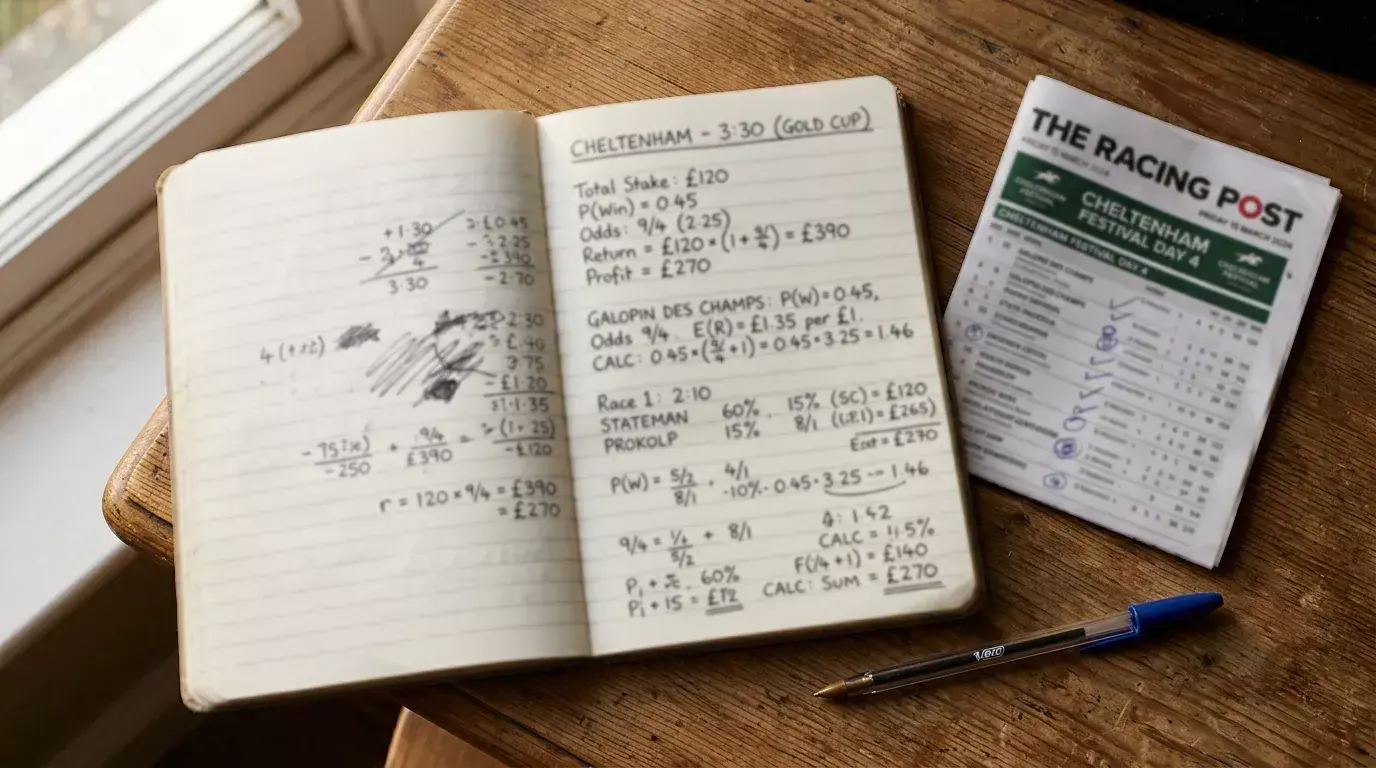

Expected value (EV) is the amount you expect to win or lose per bet over the long run. The formula is: EV = (probability of winning x profit if you win) minus (probability of losing x stake). If EV is positive, the bet has value. If it is negative, the bookmaker has the edge.

Here is a worked example. You assess a horse’s true probability of winning at 25%. The bookmaker offers 5/1 (decimal 6.0), which implies a probability of 16.7%. A ten-pound bet at 5/1 returns 60 pounds if it wins (50 profit plus 10 stake). The EV calculation: (0.25 x 50) minus (0.75 x 10) = 12.50 minus 7.50 = plus 5.00. That means every time you place this bet, you expect to make five pounds in the long run. The horse will lose three-quarters of the time, but when it wins, the payout more than compensates.

Now flip it. Same horse, but the bookmaker offers 3/1 (decimal 4.0), implying 25%. Your assessment is also 25%. EV: (0.25 x 30) minus (0.75 x 10) = 7.50 minus 7.50 = zero. No value. The odds exactly reflect the probability. And at 2/1 (decimal 3.0), the EV turns negative: (0.25 x 20) minus (0.75 x 10) = 5.00 minus 7.50 = minus 2.50. The bookmaker has the edge.

The entire discipline of value betting rests on this calculation. The difficulty is not the formula — it is the input. Your estimate of the horse’s true probability is the variable that determines everything, and getting that estimate right is where skill, form analysis and experience converge.

Identifying Overlays: Tissue Prices vs Market Prices

An overlay is a bet where the market price exceeds what you believe the true price should be. The term comes from the concept of “tissue prices” — the set of odds you would create if you were making the market yourself. If your tissue has a horse at 3/1 and the bookmaker is offering 5/1, that is an overlay. If the bookmaker offers 2/1, it is an underlay.

Building tissue prices requires assessing each horse in a race independently. I use a simplified ratings-based approach: I assign each horse a rating based on form, going preference, course suitability, jockey and trainer data, then convert those ratings into percentage probabilities. The probabilities must sum to 100% (or close to it — a margin of two or three percent either way is acceptable). From those probabilities, I derive my tissue prices.

The comparison between tissue and market is where overlays surface. In a ten-runner handicap, I typically find one or two horses where the market price significantly exceeds my tissue price. Those are my bets. Betting turnover per race fell 5.6% year-on-year in 2025 — that contracting liquidity can sometimes create wider pricing gaps, particularly in the less popular meetings where bookmakers set their lines with less granular data.

A common mistake is to assume that longshots are inherently better value than favourites. They are not. A 20/1 shot with a true probability of 3% is poor value (implied probability at 20/1 is 4.8%, which is higher than 3%). A 2/1 favourite with a true probability of 40% is excellent value (implied probability at 2/1 is 33.3%). Value is relative to the true probability, not to the size of the price.

Why 500 Bets Is the Minimum Sample to Judge a Strategy

The losing run I mentioned at the start — 47 bets without a winner — illustrates why small samples are meaningless in value betting. Variance dominates short-term results. A strategy with a genuine positive expected value of 5% per bet can still produce a loss over 100 bets due to the natural randomness of outcomes. The mathematics of probability tell us that you need a large sample before the actual results converge towards the expected results.

The minimum sample I recommend is 500 bets at consistent stakes and consistent methodology. Below that number, you cannot distinguish between a profitable strategy and random luck — in either direction. A punter who backs 50 horses and makes a 30% profit might be skilled or might be lucky. A punter who backs 500 horses at a 30% profit is almost certainly skilled.

Record-keeping is the foundation of sample-based evaluation. Every bet needs a date, the race details, the horse, the odds taken, the stake, the result and your pre-bet probability estimate. Without the probability estimate, you cannot calculate whether your bets had positive expected value — you can only see whether they won. Winning is not the same as finding value, and losing is not the same as being wrong. The records tell you the difference.

I use a spreadsheet that calculates running EV, actual profit/loss and the gap between the two. Over 500-plus bets, those lines should converge. If your actual profit consistently trails your expected profit, your probability estimates are too optimistic. If it exceeds expected profit, you are either underestimating your edge or running well. Either way, the data tells you where to adjust — and it only tells you anything useful after you have accumulated enough bets to drown out the noise of short-term variance.